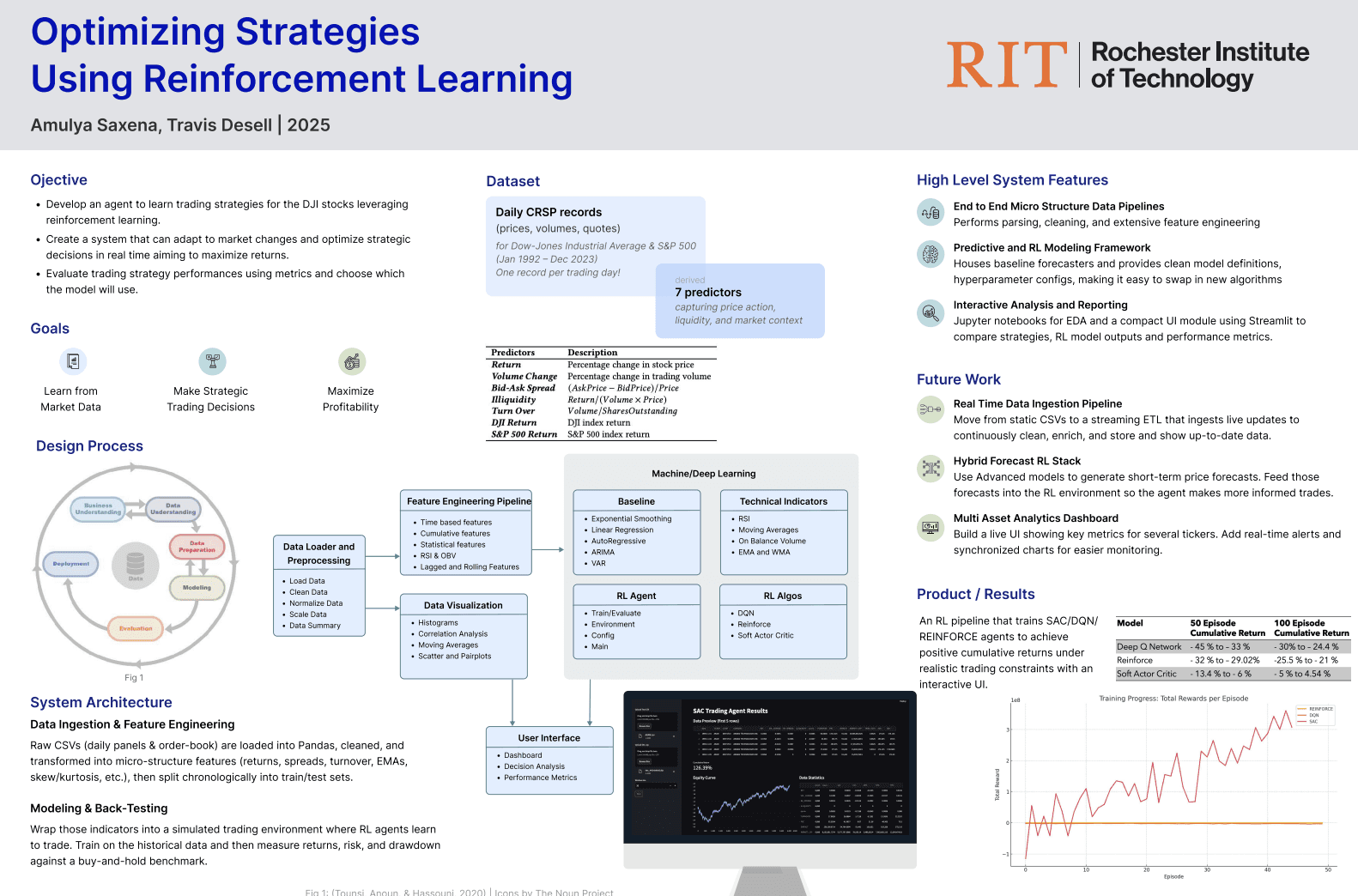

This capstone investigates whether deep-RL agents can reliably outperform conventional factor-based strategies on U.S. equities when realistic frictions (bid–ask spread, turnover, market impact) are included.

The workflow is divided into three layers:

Layer Goal Key Artefacts Exploratory & Feature Engineering Clean market micro-structure data, engineer lagged / rolling factors Data/, DataPipelines/ notebooks & scripts Classical Baseline Benchmark with Random Forest, SVR, ARIMA forecasts ProjectCode/baselines/ Reinforcement Learning Train DQN / PPO agents inside a custom Gym environment that emits (state = engineered features) and rewards (risk-adjusted PnL) ProjectCode/rl_env/, ProjectCode/train.py, ProjectCode/evaluate.py